LENDING

How to Find Creditworthy Borrowers

Contents

In the lending business, the borrower’s intention to repay is much harder to assess than their ability to repay. However, determining creditworthiness is crucial for mitigating the financial risks of your business.

In this article, we will discuss a few strategies that can help you find creditworthy borrowers.

Let’s get started.

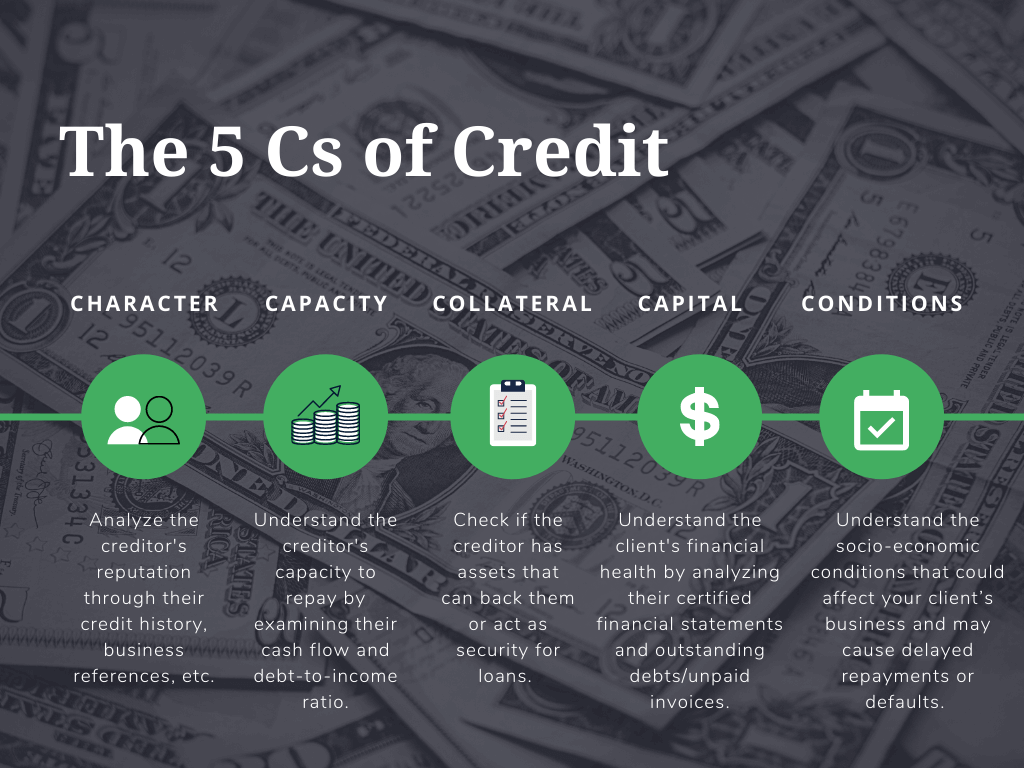

You can use the 5 Cs of credit for assessment.

For example, by 2030, about 50% of Indian automobiles will go electric. It will bring a massive change in the automobile sector. Electrical engines will boost business for companies that create electric components. But it will also bring down the number of diesel and oil-based engines, and maybe the business for OEMs if they don’t transition with the market demand.

Therefore, you must assess the borrower’s profile thoroughly and consider the surrounding conditions before lending.

However, a common challenge in lending business is to collect and map the information from several sources securely. You can use Lending CRM to compile borrowers’ profiles from multiple sources and data exchange APIs, such as LOS, CIBIL, Experian, Perfios, and NetBanking Connect.

Another challenge is to manage the client’s documents and ensure that all teams (verification, underwriting, collections) have the same updated copies of the documents. Also, if the customer is not eligible for loan, the lender has to communicate the same in a timely manner.

A simple way to resolve the above challenge is to provide your clients a self-serve loan portal, where they can easily apply for loans, manage their profiles and applications, upload documents, check application status and receive verification & approval notifications.

Your internal teams can also access the documents in real-time and decide the creditworthiness of a client instantly.

LeadSquared helps us manage our lending partnerships with banks & NBFCs, and our internal processes across the lending lifecycle (sales, credit, verification & operations) to disburse loans 30% faster than before.

Anuj Sachdev, while working as VP – Product, Qbera (now acquired by InCred)

Let’s move on to the next aspect of determining creditworthiness – credit risk analysis.

In 2008, commercial banks, investment banks, and other financial institutions underestimated the credit risk, which resulted in loan defaults and the great recession the world has ever seen.

Lesson learned: determining creditworthiness beforehand is essential for a sustainable business.

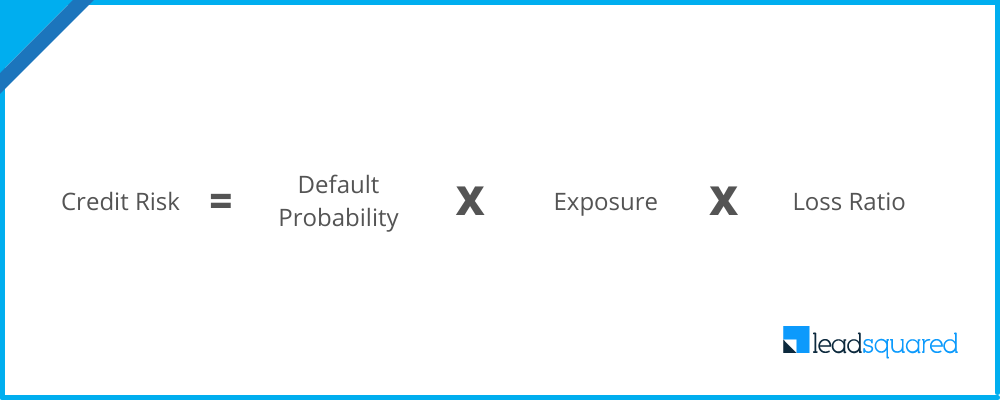

How to determine credit risk

When an individual applies for a personal or business loan, the bank or financial institution must analyze the potential benefits and costs associated with the loan.

Credit risk analysis is an easy way to understand the possible loss from any financial transaction. It is calculated as:

Where:

Note that new age lenders also use advanced, computerized credit risk analysis models to improve the accuracy of credit risk predictions.

The purpose of credit risk analysis is to analyze the risk factors and minimize losses due to defaults.

Thankfully, technology is making it easy to find creditworthy borrowers. For instance, you can create rejection filters on your Lending CRM to eliminate the profiles that you cannot lend to.

Due to pre-screening automation, we are able to reject files right at the onset. By doing that we are able to improve our main funnel quality by 60 to 70%. Only the quality data moves to the core underwriting process, and our underwriting bandwidth is not getting choked.

Vaibhav Maheshvari, Former AVP, Profectus Capital

Typically, banks and financial institutions would try to figure out a person’s intentions through face-to-face or personal interactions. In such cases, the judgment to lend or not relied on the lender’s experiences. Lenders would consider their cultural makeup and values in their decision to lend. But this system would limit the lender’s services to specific geography.

While many lenders still follow a similar approach to assess borrower’s intention to repay, technology such as video KYC and eKYC have made it easier for verification teams to converse with the borrowers – irrespective of their location.

The above methods will help lenders gain confidence that the borrower will honor their debt obligation and repay as per the agreed timeline.

The new-age lending companies are actively using digital tools to automate their processes. Technology, no doubt, has made assessing creditworthiness easier. Here are the 5 such examples.

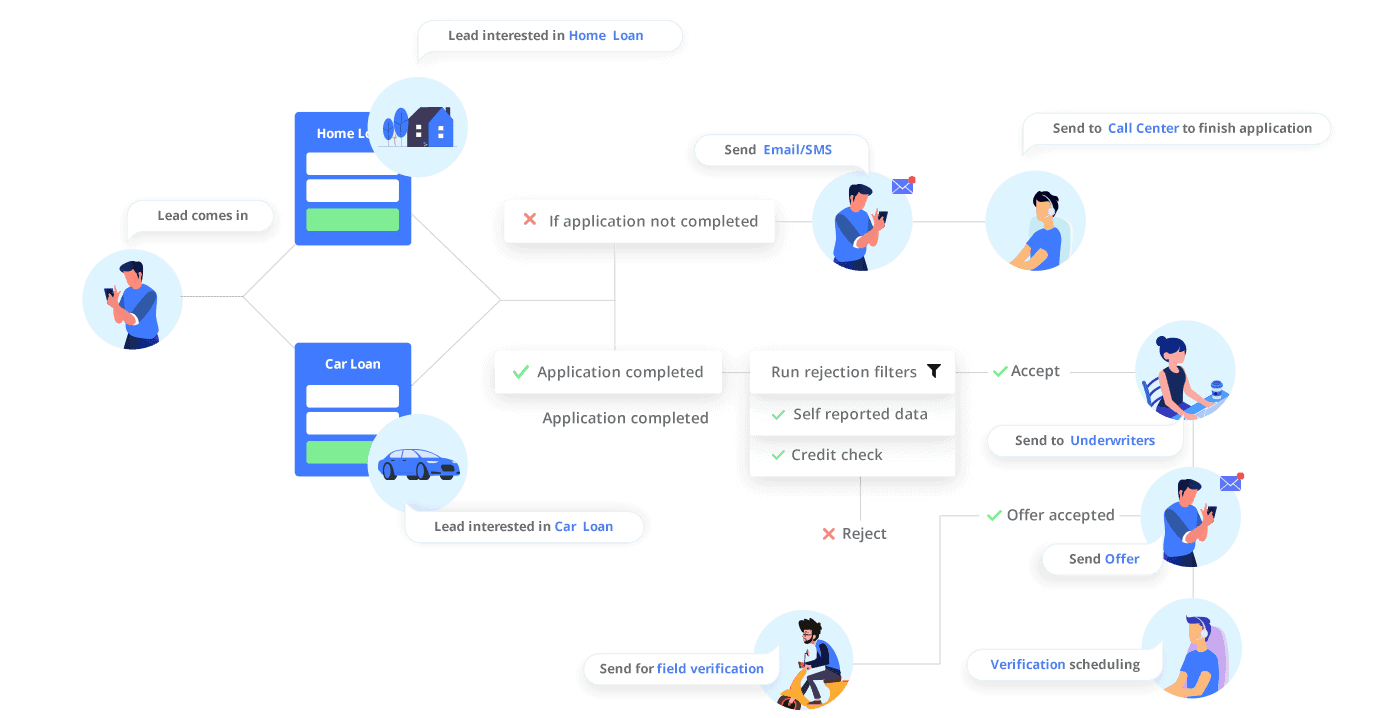

IndiaLends is a digital lending marketplace that connects consumers and small businesses looking for low-rate loans with institutional lenders looking for good returns.

On a high level, their operational model involves:

Some of the use cases fulfilled by LeadSquared Lending CRM for IndiaLends are:

Finnable Credit Pvt. Ltd. is one of the fastest-growing fintech start-ups in India. Their goal is to make personal loans available to salaried professionals in less than 1 minute.

As they have to disburse loans within a very short time, they use automated workflows for document collection, background verification, underwriting, and loan disbursal.

Every team in the organization – from sales to underwriting and disbursal teams – uses LeadSquared. The team sees LeadSquared as a front-end LOS system, to not only map the customer journey but also to provide customer support.

Arif Hassan, Head – Customer Experience, Finnable

Read the complete case study.

Finance Buddha is an online marketplace for retail finance. They provide a range of secured lending products, including mortgage loans, SME loans, and personal loans for salaried and self-employed individuals.

For every new loan inquiry, they use Lending CRM to check a basic set of fields before they match the lead with a suitable vendor. The system analyzes the lead score and qualifies them. Only qualified leads are mapped to a vendor.

With this simple automation, they are able to serve 30% more customers.

Read the complete case study.

Profectus Capital is a non-banking financial services company. They offer loans primarily to the manufacturing and service sectors. They also provide supply chain financing solutions to high turnover industries such as automobiles, pharmaceuticals, and consumer durables.

Profectus uses LeadSquared for their sales activities, lead capture, lead engagement, pre-screening, and sales monitoring. They also use the Mobile CRM for field operations such as offline verification and document collection. The tool integrates with their Loan Origination System (LOS) through which applications are verified. Then based on email and mobile OTP verification and CIBIL score, only qualified leads are sent for underwriting.

Read the complete case study.

Qbera is a new-age lending firm empowering the employees to get personal loans digitally. Qbera has built technology to make instant lending decisions. With this, they can disperse loans in as little as 8 hours.

Qbera follows a paperless application process, and they need to verify that the customer wants/needs the loan. They confirm the application through SMS and IVR. Then, the application is sent to the risk assessment team for verification. All these processes are handled through LeadSquared Lending CRM. Their DSAs (Direct Sales Agents) also use LeadSquared’s mobile CRM for field cases.

Read the complete case study.

The definition of creditworthy depends on the lender’s risk appetite. For instance, some lenders may be okay to give loans to clients with a lower credit rating, while others may not.

Nonetheless, you can use software tools such as Lending CRM to make your lending process more efficient – from finding creditworthy customers to loan disbursal and collections.

Lending today has become a lot more scientific rather than being a pure art form.

KV Srinivasan, Executive Director & CEO, Profectus Capital

CIBIL score is a numeric interpretation of a person’s credit history over a specific period of time. It ranges between 300 and 900. Lenders generally consider CIBIL scores and other information for determining the creditworthiness of a customer. Here’s the link to the free CIBIL score calculator.

Some of the popular credit scoring systems are FICO (Fair Isaac Corporation), TransUnion CIBIL, Equifax, Experian, and CRIF Highmark.

Enter your details and we'll send you a quick confirmation email to verify your address.

How to Create Highly Useful College Student Personas

How to Create Highly Useful College Student Personas